Beyond the obvious difference of combining the HTML and XBRL, iXBRL requires a transition to XHTML and thus introduces some technical differences about which you should know. For example, some HTML tags, such as <font> tags, and certain HTML attributes like ”name” are no longer valid. Rather than <font> tags, XHTML requires the use of a <span> element, and the HTML attribute (name=“example”) should be represented with a unique ID attribute (id=“example”) instead. Furthermore, the closing tag is essential in XHTML. For example, HTML does not require <hr> element to have a closing tag, however, that would be invalid XHTML. For that element to be valid, a self-closing <hr/> tag is required. Another area where the technical differences are apparent is regarding numeric character references and a character entity references. There are only five entity codes that are allowed in XHTML, and they can be found below.

Character Reference |

Special Characters |

Description |

|

< |

< |

Less than |

|

> |

> |

Greater than |

|

& |

& |

Ampersand |

|

" |

“ |

Double quote |

|

' |

‘ |

Single quote |

|

Allowed entity codes in XHTML |

||

When converting from HTML to XHTML, any character entity references not listed above should be converted to their equivalent numeric character reference. For example, the Dollar sign ($) does not have a non-numeric entity reference, therefore the numeric character of ($) is required.

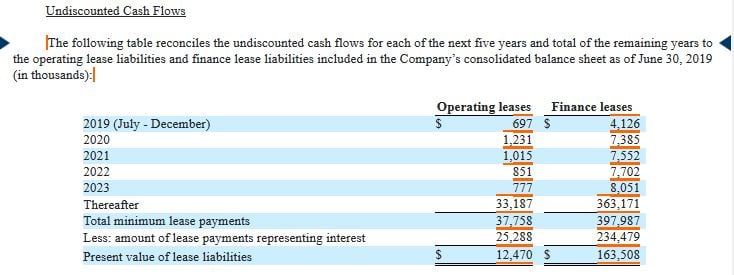

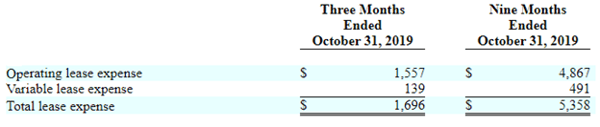

To fully illustrate differences in more detail, we will compare how one number is included in the filing in HTML/XBRL compared to iXBRL. Let us track the number reported as the Operating Lease Expense for Three Months Ended 10/31/2019, 1557, which is scaled to thousands.

HTML Table |

|

| This table provides an example of a human-readable format as it appears in HTML |

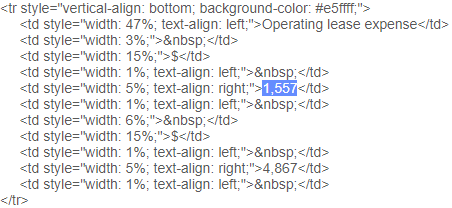

HTML Snippet |

|

| Here you can see the underlying HTML tags used to format and present the number |

XBRL Snippet |

|

| Here you can see the underlying XML tags used in the XBRL instance document to represent the number |

Derivation of the iXBRL |

|

| Here you can see that the XBRL tags are embedded in the HTML tags, combining both the presentation and the financial tagging information |

Viewed in the Inline Renderer |

|

| Because iXBRL is the combination of HTML and XBRL, when viewing the filing in the SEC Inline Renderer, we see the HTML presentation along with the XBRL information; reducing and simplifying the review process. |

One of the most complicated aspects of building an iXBRL filing is understanding how data transformations within the filing work. These transformations change a value from the HTML into the proper iXBRL format required by the SEC. The transformation used for each fact is listed within its detailed fact popup in the SEC Inline Renderer and due to the standardization of the outputs, it simplifies comparing facts. Although these data transformations are often found on the filing’s cover page, they can be used throughout the filing as well.

Cover Page |

|

|

An inline preview of a tagged 8-K cover page. |

Transformations are listed in the SEC’s EDGAR Filer Manual and are defined and approved by XBRL International or the SEC. As iXBRL evolves, future versions of the EDGAR Filer Manual might introduce more data transformations.

Here are some common examples of data transformations:

durwordsen: This will transform duration words, such as “five years”, into “P5Y”. It is a way of standardizing durations so that they can be easily compared.

duryear: Similar to durwordsen, duryear will take a duration format that uses numbers rather than words for the number of years and turn it into the same comparable format. For example, “5 years” would transform into “P5Y”.

datemonthdayyearen: This changes the common date format, “December 31, 2019”, into the computer readable date format, “2019-12-31”.

boolballotbox: This transformation changes the Unicode ballot box characters (“☐”, “☑”, “☒”) from symbols to the corresponding values of “true” and “false”.

stateprovnameen: This will transform the name of a state or province into its 2-letter code, for instance, “Delaware” will transform into “DE”. A common issue here is that it only allows for the first letter to be capitalized, so “DELAWARE” would result in a hidden fact and test filing warning. One way to work around this issue is to change the HTML to use the text-transform attribute to make the word appear as capitalized but have the underlying text in lowercase.

Although data transformation makes it easier to compare facts, there are issues that filers may encounter. One issue a filer might run into is a fact that cannot be transformed due to the currently allowed rules. In this situation, the fact will be marked hidden while still providing a link to the associated text in the Renderer. For example, the text “6-months” tagged with a duration data type will be marked hidden. Due to the hyphen, the fact cannot be transformed into the iXBRL format, but it would still be linked in the filing.

Additionally, filers may run into test filing warnings, such as Hidden-Fact-Eligible-For-Transform, if there is an eligible data transformation for a concept but not being utilized due to text formatting or other inconsistencies. Although this warning may imply that the filing was generated incorrectly, in some cases this is unavoidable. For example, if the value for EntityIncorporationStateCountryCode in the HTML document is set in all caps, e.g., NEVADA, the fact would be linked but the filer will receive a Hidden-Fact-Eligible-For-Transform test filing warning. One way to work around this issue is to change the HTML to use the text-transform property in CSS to make the word appear as capitalized in the filing but have the underlying text in lowercase.

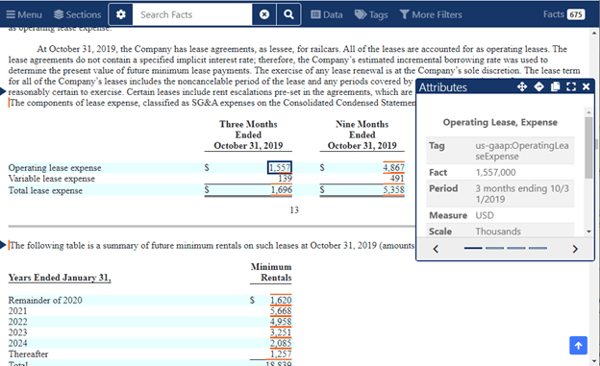

In addition to the amendment to require filers to transition to iXBRL, the SEC released an open-source iXBRL visualization tool to preview how filings would render once filed. The SEC’s Inline Renderer takes iXBRL files and renders them in a way that is easy to review. Because the XBRL data is embedded directly into the HTML document, the Inline Renderer will allow the user to see the rendering on a web browser with a marked-up version of the original HTML.

The Renderer is available for anyone to download and install on their personal computers from the Arelle website. Their documentation page includes step-by-step instructions on how to install and use the renderer, which can be through a graphical user interface or the command line.

The Inline Renderer will allow the user to see the original HTML formatting with orange markups for each particular fact. The orange markups highlight facts that have more details about the iXBRL tag used. Text block and table text block-level tags will have a vertical orange bar before and after the fact which can be clicked on for more details regarding the iXBRL tag.

Orange Fact Markups |

|

|

The header bar of the Renderer offers several helpful tools. For example, the Sections option allows the user to jump to different sections of the document. It offers a similar function to the standard sidebar of the XBRL Renderer. The new Inline Renderer also features a search bar which is useful for looking up concepts, values, or text within the document. The search feature also comes with a filter, allowing the user to set different searching parameters such as fact name, definition, or dimension. Lastly, the Data, Tags, and More Filters found on the header bar offer additional filtering capabilities of the rendering.

Inline Renderer Header Bar |

|

|

This new way to render an iXBRL filing comes with a few complexities. One complexity is with hidden facts. Some facts do not have text within the HTML filing that can have a direct link. Therefore, to view these facts in the preview, the user has to filter by Additional Items Only which is located under the Data dropdown and opening the fact sidebar on the right-hand side. An example of one of these facts is the Entity Central Index Key, which is still required to be tagged within the filing but is not listed in any text within the filing.

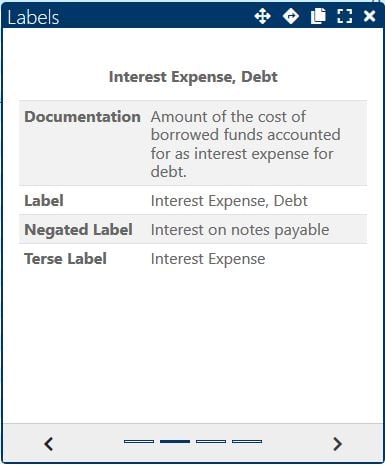

Another complexity is how the Inline Renderer displays label information. For each fact within the pop-up window, there is a tab for Labels.

Labels in Fact Dialog |

|

The tab lists all the labels that were used for a specific concept throughout the entire filing, including any standard, negated, terse, or verbose labels, but does not specify which type of label was used for the fact that is currently being viewed. This issue may cause confusion because without looking at the underlying iXBRL, there is no way to know which of these labels was used in this context.

Another complication that was introduced with iXBRL is the usage of continuations. Continuations are used when a fact spans over several nonconsecutive paragraphs or sections; the “ix:continuation” tag is used to connect the sections to each other and assign the same concept. This is common for text block sections to avoid page breaks or unwanted whitespace. Each of these continuation tags must link to one another, and if just one of the links is broken or incorrect, the entire chain would be incorrect.

Amin Kassim is a Business Analyst at CompSci Resources, LLC. He earned a M.S. in Analytics from American University. Here at CompSci, he is responsible for preparing and processing SEC filings for public and investment companies. By leveraging our patented technology, Amin Kassim helps businesses comply with SEC requirements.

![]()

Amin Kassim

Business Analyst at CompSci Resources, LLC